Every successful agent knows his or her role is more than pitching products—it’s about bringing real, measurable value to the dealer every day. The best agents step into a store, not just with a briefcase of contracts, but with solutions for the margin compression that’s hitting every rooftop. Margin compression today isn’t about only vehicle pricing; it’s fueled by claim severity, higher frequency of losses, and skyrocketing repair costs.

An agent’s day often starts with analyzing the dealership’s performance data: per-vehicle-retail trends, product penetration, and loss ratios. This groundwork is how agents identify the pressure points. For example, if rising service claims are eroding profitability for the dealer’s reinsurance company, the conversation shifts toward how additional protection products can stabilize the portfolio, feed reserves back into the reinsurance structure, protect customer satisfaction index, and secure customer retention.

The agent’s job is to transform these numbers into objective value—coaching F&I managers, refining menus, and providing training that ties directly back to profitability and long-term dealer wealth.

Why ‘Now’ Makes the Most Sense for Consumers

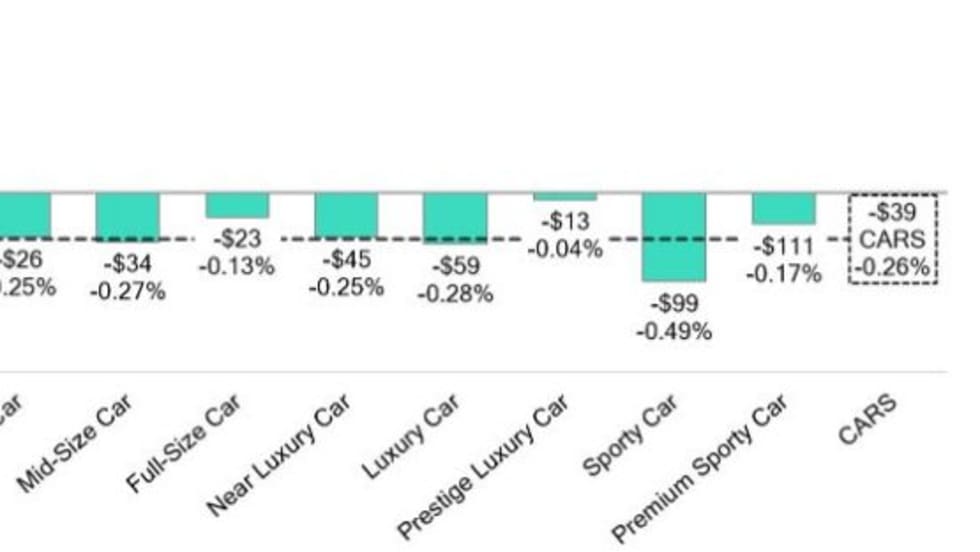

Inflation isn’t just showing up at the grocery store. The average cost of vehicle repairs has jumped double digits since 2020. Parts inflation, labor shortages, and technology-heavy vehicles have pushed claim severity to all-time highs. What does that mean for consumers? The cost of going “unprotected” has never been higher.

Consider these realities:

The nationwide negative equity average recently hit $6,500. That means customers are walking into dealerships already upside down, making gap protection more critical than ever to shield them from financial strain if their vehicles are totaled or stolen.

A $3,000 extended service contract looks very different when the average transmission replacement exceeds $6,000.

Tire-and-wheel protection is no longer optional when a single rim can cost more than $1,200.

This is where agents carry the torch for purposeful conversations. Instead of selling “another product,” the dialogue becomes about peace of mind and smart ownership.

Case Study: Purposeful Conversations in Action

Just last week, I worked with a finance producer at a high-line store who was delivering a preowned BMW M4. The younger buyer was rolling over negative equity, with Dad as a co-signer, and the loan advanced at 130% loan-to-value ratio. The F&I manager initially said there wasn’t room for gap unless the customer brought additional cash. The customer’s response?: “I don’t see the value. I don’t need gap.”

This is where purposeful conversation changes the trajectory. I had the manager pull Edmunds’ “True Cost to Own,” which showed the car was projected to depreciate another $13,000 in the first year, on top of the customer paying 11% interest. Put simply, if someone else crashed into him, resulting in a total loss, he would still owe north of $25,000 on a car he no longer owned.

The F&I manager took that story back to the lender, secured an additional advance, and the customer’s payment went up just $17 a month. When presented with the reality, the customer instantly wanted gap.

The result? Doing the right thing by the customer, protecting him from potential financial ruin, while also adding $700 in profit to the deal—and perhaps more importantly, the finance producer learned a new mindset and process for presenting value. That’s what purposeful conversations look like.

From Transactional to Relational: Rebuilding Trust After COVID

The pandemic created an “ultra-transactional” marketplace. Vehicles were scarce, demand was high, and conversations often stopped at “take it or leave it.” Dealers captured short-term profits, but long-term retention took the hit.

Now as the dust has settled, customers are again looking for trust and relationship. Agents play a crucial role in reshaping that approach. By training F&I professionals to ask deeper questions—“What concerns you most about ownership?” or “How long do you plan to keep this vehicle?”—the conversation pivots from pressure to purpose.

But it doesn’t stop there. It’s about getting personal—understanding who the customer is, learning their “why,” discovering what’s important to them. Building a genuine relationship with trust, and even laughter, helps people truly connect. This is not about handing out word tracks or memorized objection handlers. It’s about delivering real-world value, supported by facts, third-party resources, and a sincere desire to protect the customer’s financial well-being.

This isn’t just good practice; it’s good business. Dealers who re-center their culture around purposeful conversations see stronger retention, higher CSI scores, and more predictable profitability.

The Agent’s Equation for Growth

When you put it all together, the PVR growth equation for agents looks like this:

Margin compression, plus inflationary pressures, plus purposeful conversations equals long-term dealer profitability, reinsurance growth and customer retention.

It is also paramount to find a wealth-management partner to help drive growth on investment income in the reinsurance company. One thing I have found is that when you work with an esteemed CPA or certified financial planner with reinsurance investment policy statement management experience, it is the absolute game-changer. Too many “big box” administrators default to big-name banks that park a dealer’s money in money market positions, U.S. bond aggregates, or other cash-type accounts. This is a massive way to differentiate yourself—by ensuring a dealer’s reserves are actually working for him or her.

When looking at the definition of agency—the capacity, condition or state of acting or exerting power—it’s clear what our role really is. It means not being tied down to one option or forcing a one-size-fits-all solution into a square-peg hole. It means asking the right questions to uncover the current strategy, pain points, profit leaks, and long-term goals. From there, the agent can act as a true steward—treating the dealer’s strategy, wealth management, and profitability as their own, and doing so with excellence.

The role of the modern agent is to bring clarity to complexity. To take the challenges of margin compression, claim severity, and negative equity, and turn them into opportunities for protection and retention. To coach dealers out of transactional habits and back into customer-first strategies. And above all, to show that in this market, protection products aren’t optional. They’re essential for both the customer’s financial security and the dealer’s long-term wealth.

When you do this, you don’t just help your dealers. You create your own economy and build raving fans.

DIG DEEPER: The California CARS Act: What Agents Need to Know

Chad Staples is president of Elevation Dealer Services, where he helps U.S. automotive dealers maximize profitability through strategic F&I programs, reinsurance structures, and long-term wealth-building strategies. He also leads modern, relationship-based F&I training.

EDITOR’S NOTE: This article was authored and edited according to Agent Entrepreneur editorial standards and style. Opinions expressed may not reflect that of the publication.